Consumer financial services providers face an evolving legal and regulatory landscape in 2021. In a recent webinar, members of Venable's Consumer Financial Services team examined the current state of federal and state consumer financial protection law and policy and outlined what companies need to know about what's ahead. The speakers shared their experiences from the front lines and offered strategies to help navigate the evolving legal and regulatory landscape.

The discussion has been condensed for brevity and clarity.

What can the House of Representatives and the Senate accomplish in this new term and what will be the impact on the consumer financial services industry?

The House has very narrow Democratic majority—more narrow than last Congress—and has reelected Nancy Pelosi as speaker. The Senate is evenly split, with Vice President Kamala Harris serving as the tie-breaking vote. Congresswoman Maxine Waters continues to chair the House Financial Services Committee, and Senator Sherrod Brown takes the reigns of the Senate Banking Committee. Those are the two committees with primary oversight of the Consumer Financial Protection Bureau (CFPB). New faces in leadership and on key committees include Representative Cathy McMorris Rodgers as ranking member on the House Energy and Commerce committee, which is key for financial services companies in addressing privacy issues and oversight of the Federal Trade Commission (FTC). Senator Pat Toomey remains as ranking member on the Senate Banking Committee.

The Senate can now

- confirm all of President Biden's agency nominations, which need only 51 votes

- rescind some of President Trump's actions, using the Congressional Review Act

- utilize the budget reconciliation process to advance legislation

The ability of Congress to approve the slate of President Biden's nominations is noteworthy; Rohit Chopra has been nominated to lead the CFPB Chopra will encourage a multifaceted approach to consumer finance issues, and return to robust enforcement. Chopra's nomination also opens up a Democratic seat on the FTC.

What are some priorities at the federal agencies tied to consumer financial services?

Key areas of focus for the CFPB will be to

- reestablish the Office of Fair Lending;

- a renewed focus on enforcement, including UDAAP and disparate impact; rule-writing in the areas of small dollar lending, possible tweaks or a stay of some or all of the debt collection rule, HMDA, and small business data collection;

- enhanced scrutiny of student lending, auto lending, and Military Lending Act compliance; and

- picking-up unfinished business and policy matters from the Cordray-era.

The federal banking agencies—the Federal Deposit Insurance Company (FDIC), Office of the Comptroller of the Currency (OCC), and the Federal Reserve Board will prioritize:

- financial inclusion

- safety and soundness

- climate change

- social responsibility

- fintech

Consumer lending priorities include

- CFPB's renewed focus on student loan servicing and short-term loan installment

- OCC's true lender/Madden rules

The diverse industries related to payments will also see priorities shift under the new administration. Looking ahead, this might include:

- new anti-money-laundering rules in place in early 2021; new beneficial ownership rules; updated cryptocurrency rules

- working toward making faster payments a reality; services are accessible only by banks at the moment, but work is being done to bring faster payments to consumers

- renewed focus on law enforcement and holding payment processors accountable in wrongdoing/unlawful conduct

Also, the Supreme Court is set to decide whether Section 13(b) of the FTC Act, which expressly grants the FTC the right to obtain "a permanent injunction," also grants the FTC the authority to obtain "equitable monetary relief." During oral argument, certain Justices expressed doubt that the plain language of Section 13(b), when viewed in the context of the entirety of the FTC Act, authorized the FTC to obtain "equitable monetary relief" when proceeding under Section 13(b). If the Supreme Court does close the door on the FTC's ability to seek equitable monetary relief through Section 13(b) in federal court, the FTC will not be defunct. However, Congress and the FTC's response will be important to watch.

Additionally, marijuana and CBD banking and payments are an area to watch, as are prepaid cards. The CFPB's prepaid rules are being challenged; at end of 2020, two parts of the agency's Prepaid Rule were invalidated. The CFPB may appeal this decision.

What changes are included in the CFPB's new debt collection rules?

In areas related to debt collection, the CFPB recently enacted new rules for third party debt collectors to go into effect in November 30, 2021. The new rules address electronic communications, harassment or abuse allegations, and false or misleading practices. Specifically, in October 2020, the CFPB released a final rule regarding debt collection communications, and in December 2020, the CFPB released a final rule on consumer disclosures. Together, the two rules amend Regulation F, which implements and interprets the Fair Debt Collections Practices Act (FDCPA). The new rules are based primarily on the Bureau's authority to issue rules to implement the FDCPA and, consequently, covers debt collectors, as that term is defined in the FDCPA.

The new rules are a major development for all participants in the debt collection market and will have a direct impact on enforcement investigations, supervisory examinations, and litigation.

Key takeaways in the new CFPB debt collection rules include:

- time and place restrictions

- opt-out clarification

- call frequency violation clarification

- email and text-allowable activities

- social media regulation

- clarification of voicemail allowances

- disclosures related to oral communications, initial communications, translation requirements, and validation notices stating that disclosures must be made consistently in the same language

- sales restrictions on paid debts, records retention requirement, credit reporting limitations, and time-barred debt restrictions

Items of note not in the new rules include:

- time-barred debt notices

- safe harbor for meaningful attorney involvement

- certain E-SIGN Act consent requirements

Collectors and creditor customers have – unless new leadership or Congress takes action to delay or rescind - less than a year until the rules take effect. Technicalities around safe harbors need to be carefully considered, implemented, and trained on.

Now, with the changeover in administration there's a lot of speculation as to the fate of the new debt collection rules. And, we also know that Rohit Chopra previously indicated support for first party debt collection rules.

"Several years ago, when the CFPB launched a rulemaking on third-party debt collection, the agency indicated that it planned to address first-party debt collection on a separate track. Despite support for this approach, it never did. Commonsense rules for ensuring accuracy in the collection and sale of debt would cut off at the source abuses like those seen in this case."

Rohit Chopra, In the Matter of Midwest Recovery Systems, Federal Trade Commission File No. 1923042 (Nov. 25, 2020). As a result, we expect this to be an area with continued rulemaking activity, and ongoing regulation enforcement by regulation.

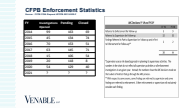

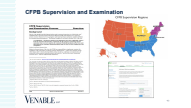

What is the CFPB's examination and enforcement outlook?

- Supervision regions remain the same for examinations. There will be renewed agency interest in student loan servicing and fintech, renewed focus on fair lending, COVID-19-related exams on servicing and collecting practices, and military lending (CFPB backed off in the last few years)

- Enforcement—the following are some areas of focus:

- Pipeline is relevant as things are decided—early announcements will span administrations

- CFPB is enforcement capabilities are fully operational

- Except to see aggressive use of UDAAP authorities

- Many companies not under supervisory authority of CFPB could be a focus moving forward

Will there be any changes to state regulatory actions?

"Mini-CFPBs"—regulatory agencies at the state levels—were initially seen as potentially sidelining the federal work of the Bureau, but these state agencies, notably those in California and New York, have proved effective.

The industry will continue to see a shift in multi-state licensing agreements as these continue to develop.

What type of takeaways do you expect?

The panelists concluded the webinar with these final takeaways:

- In the payments sector, enforcement agencies can still do lookbacks, and there will be a renewed emphasis on looking for "chokepoints."

- Businesses should expect more examinations and investigations looking ahead.

- On the legislative front, congressional hearings will likely be better coordinated with federal agencies. Regulatory appointees will have a long-term impact.

- In 2021 and beyond, the innovation office at the CFPB is an area to watch, with compliance and consumer protection playing important roles in this space.

- For compliance efforts, sweat the details on technical compliance, and also focus on prohibitions on unfair, deceptive, or abusive acts and practices. Revisit the Cordray-era Supervisory Highlights, and expect to the enforcement department to push the boundaries.

* * * * *

Want to learn more? View the full webinar, or explore our Consumer Financial Services practice page.

Related articles and presentations:

Online Lending Legal and Policy Issues Resources

President Biden Selects Rohit Chopra to Lead CFPB and Appoints Acting Director

Court Vacates Two Provisions of the Prepaid Rule

Final Debt Collection Rule Issued by CFPB

Understanding the CFPB Debt Collection Final Rule

Debt Collection Consumer Disclosure Rule

Five Common Consumer Financial Services Legal and Regulatory Due Diligence Mistakes to Avoid in M&A

What's Inside the CFPB Enforcement Policies and Procedures Manual