The Legislation

On October 5, 2018, the president signed Public Law 115-254 into law – the Better Utilization of Investments Leading to Development Act of 2018 (BUILD Act). The BUILD Act creates the United States International Development Finance Corporation (IDFC), a new wholly owned government corporation. It will replace the Overseas Private Investment Corporation (OPIC) and transfer, among other functions, the Development Credit Authority from the U.S. Agency for International Development (USAID) to the IDFC. It is subject to reauthorization in seven years.

The most important new authority under the BUILD Act, and the focus of this article, is the authority of the IDFC to place equity investments pursuant to Title II, Section 1421(c)(1). Currently, OPIC is strictly limited to debt issuance and political risk insurance, so this significant new expansion into equity puts the IDFC at the limited partner table for the first time. The IDFC's aggregate equity support will be limited to (i) five percent (5%) of the IDFC's overall contingent liability in any one entity, (ii) thirty percent (30%) of equity invested in any one project, and (iii) thirty-five percent (35%) of the IDFC's overall contingent liability. The BUILD Act doubled the contingent liability cap for the IDFC from $29 billion to $60 billion, which means approximately $21 billion in new limited partner commitments will be available from the IDFC that did not previously exist in the marketplace. This is great news for corporate recipients and equity funds in emerging markets worldwide, but it will take time for the IDFC to build its equity investment operations.

Why Equity, Why Now

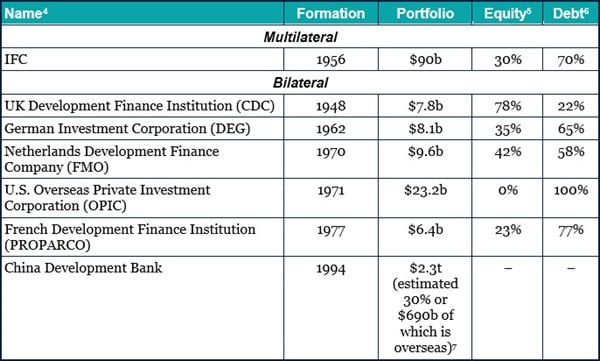

Most development finance institutions (DFIs) began as loan-making institutions from the 1940s to the 1970s. However, three things have changed. First, private capital flows into emerging markets accelerated in the 1980s, so many DFIs began to build equity programs then. It took decades to build them because DFIs were learning the equity business, but they are now proficient and substantial operations. Second, foreign direct investment (FDI) has largely replaced official development assistance (ODA). ODA represents only 15% of cash flows into emerging markets today, but commitments from DFIs to the private sector under the auspices of FDI have jumped by about seven times, from $10 billion in 2002 to $70 billion in 2014.1 Third, where international financial institutions and western governments traditionally served as the only donors for emerging markets, emerging economies are becoming lead suppliers of development finance to strengthen south-to-south relations. The China Development Bank in particular, under its "going out" policy, has far surpassed the world's largest multilateral DFIs combined, including the International Finance Corporation (IFC), with around $2.3 trillion on hand, a third of which is overseas, making it a significant competitor with western DFIs.2 OPIC has not kept pace with the more competitive, market-driven approach to investments in emerging markets over the past 30 years and has missed investment opportunities because of its singular debt operation. It is a stand-out among DFIs, as seen in the table below:

As a result, Congress and OPIC have advocated for the expansion of OPIC for years to better compete with DFIs from the G-8 and East Asian countries, particularly China. The BUILD Act should do that because the IDFC will have broader product offerings that include equity, and reduced fragmentation, which should improve policy coordination and policy alignment and increase operational efficiencies for cost savings to the U.S. taxpayer. However, like its European counterparts, expect the IDFC to take time in getting its equity division up and running.

Operational Considerations

No later than February 2, 2019, the president was supposed to have submitted a reorganization plan to Congress detailing the transfer of agencies, personnel, assets, and obligations to the IDFC. As of the date of this report, the recent government shut-down delayed submission of the reorganization plan and we have not seen reports that the reorganization plan has been completed and submitted to Congress. The president, the CEO of OPIC, and the administrator of USAID also must submit a joint report to Congress describing the procedures to be followed after such functions have transferred. The reorganization plan will become effective on the date set forth in the plan, but the earliest effective date is May 3, 2019, and our understanding is that it is more likely that the reorganization will occur in the fall of 2019. Until then, normal business operations of OPIC will continue.

More importantly, following reorganization, the IDFC will need to analyze how best to operationalize its equity arm. In 2017, the Inter-American Investment Corporation's Office of Evaluation and Oversight (IAIC) issued a terrific comparative study of equity investments by DFIs, which highlights five basic choices that the IDFC will need to consider, and is similar to the IAIC's own assessment of how to re-enter the equity investment space:8

- Objectives. The IDFC will first need to clarify the objectives that it wants to achieve with its new equity investment capabilities. At the outset, it might be enough that it now provides an expanded set of products that makes it more competitive. As it matures, however, the IDFC will need to weigh preferences for (a) enhancing equity access to companies, (b) enhancing equity access to funds, and (c) increasing returns as against development priorities. Many DFIs currently blend these objectives in one form or another.

- Risk Appetite. The IDFC cannot invest more than 35% of its contingent liability cap into equity investments, but it still must weigh its overall risk appetite for equity, in proportion to its overall investment portfolio of debt and equity. Equity yields higher returns, but comes with greater volatility and cost. OPIC has traditionally invested in larger-scale financings in infrastructure that have a meaningful involvement of the U.S. private sector, where USAID makes much smaller investments that are locally oriented overseas and with greater risk tolerance in a much less structured environment. The IDFC will need to bridge those two cultures and open itself to the inherently risky nature associated with equity investing. Moreover, equity puts more demands on operational resources than debt and requires long-term investee engagement and closer investment supervision. Some estimate that equity is twice as expensive as debt to administer. The IAIC notes that for each dollar committed to equity, $3-$5 of debt business must be forgone. The IDFC's risk appetite for equity ultimately will determine the scale of its equity operations and the scale of personnel, systems, policies, and procedures.

- Specialization. The IDFC will need to determine the types of investments it intends to make, be it seed funding, growth-equity, or mature-equity. The IDFC will also need to make decisions about how best to leverage its sectoral and geographic strengths. Beyond personnel who originate and structure equity transactions, the IDFC will also require individuals with (i) industry-specific and market-specific knowledge within certain geographies that can undertake proper due diligence of investments and (ii) business acumen who can function effectively within corporate governance, business operations, finance, management, and sales and marketing, and who can constantly evaluate the fair market value of any given investment target. The IDFC will need to make a concerted effort to find and hire individuals with these specialized capabilities because supervision of direct equity investments is more complex and more hands-on than monitoring loan portfolio performance. The IDFC will also need to determine how best to organize these personnel and whether they will be shared across the debt portfolio or separated into a stand-alone unit.

- Long-Term Investing. The IAIC study found that a long-term, patient perspective on equity investment is imperative to the success of DFI equity funds, and that stop-and-go investment or operating under annual approval quotas results in poor returns. In essence, the IDFC must develop and stick to a long-term equity investment philosophy that is not subject to year-to-year political bidding.

- Personnel Incentives. Debt investments typically do not involve the same level of incentive intricacies that equity investments do. The IAIC study indicates that annual approval quotas can be costly because staff are inclined to pay higher prices on investments to ensure that they meet their quota. Conversely, incentives that overly encourage long-term relationships can limit staff willingness to liquidate an investment when the valuations are attractive. The IDFC will need to structure its incentive system – perhaps with long-term performance awards – to align the goals of its investment officers with the goals of the institution, but will inevitably face perceptions that staff of a publicly supported institution should not be compensated on or benefit from the strong upside of an investment, as in the private sector. This will be an ongoing and challenging dynamic for the institution.

One of the most fundamental choices the IDFC will need to make is structuring investments as direct equity, equity in funds, or both. Most mature DFIs combine them. But during this early transition and learning phase, the IDFC may want to consider the following approach.

- First Step: Equity Funds. It might be easiest for the IDFC to start investing in equity funds first. They come at a cost because of overhead, management fees, base commissions, hurdle rates, and carried interest, and may not provide the same return rates as direct investing, but the primary basis for success is properly evaluating fund managers instead of managing the entire origination-structuring-supervision-exiting process required when investing directly in targets. Given OPIC's history of providing debt to funds and its experience with evaluating those managers, outsourcing the investment process to external fund managers might be a good natural starting point while the IDFC studies up on the equity field and equips itself with equity-experienced personnel who can create an origination process equipped to address high-churn deal assessment and inevitable conflicts of interest that will arise with pre-existing debt clients. Funds also add learning value. They can expose the IDFC to sectors and countries where the IDFC may not have presence or experience and provide an opportunity for the IDFC to learn directly from its GP investees while the IDFC readies itself for direct investments. The CDC and FMO both rely on third-party funds to diversify their equity placements. FMO places 59% if its cash with funds and only 41% in direct investments. DEG places 48% of its cash with funds and 52% in direct investments.

- Second Step: Quasi-Equity Instruments. As an intermediate step, subject to demand, the IDFC might consider issuing quasi-equity instruments that feel more like debt, because of OPIC's history and comfort with debt. For example, the IDFC might offer clients subordinated debt, convertible debt, profit-sharing debt, and mezzanine debt with warrants because of their debt-like nature. This intermediate step could help the IDFC manage its risk and reward profile. It also may offer it more time to adapt to direct investing operations as it establishes things like investment percentages sufficient for the IDFC to influence target business practices and investment holding periods long enough to enable that impact, but flexible enough for the IDFC to secure strong returns. The IAIC found that most investment percentages are 5%-20%, and most investment horizons are 3 to 10 years.

- Third Step: Co-Investments. Graduating still further, the IDFC could consider co-investing directly with other DFIs to get a first-hand look at direct equity investments without bearing 100% of the risk. It can test its experiences with new fund documentation like term sheets, purchase agreements, voting rights agreements, and shareholder agreements. The IDFC can also acquaint itself with initiating and completing investment exits. As noted in the IAIC study, however, co-investments can be challenging because DFIs typically cannot respond quickly enough together to capture investment opportunities like these.

- Fourth Step: Direct Investments. The last step entails the IDFC's first direct investments. Direct investing will work best once the IDFC has (i) an experienced, structured corps staff, (ii) thoughtful policies and procedures in place, and (iii) a clear understanding of its competitive advantages from existing relationships, local presence, or sector expertise. Direct investing will afford the IDFC greater control over its investees, but will come at a high processing cost because the IDFC will need to be fully prepared to source, structure, monitor, and exit investments in-house. The IDFC will certainly want its first few recipients to show high developmental potential and serve as a positive signal to the market that the IDFC is capable of selecting targets carefully based on competitiveness and productivity that may be worthy of additional commercial capital.

Conclusion

Creation of the IDFC and its expansion into equity investments is exciting, but will take time to build and will face challenges, not least of which is determining how to score the cost of its equity investments for congressional budgetary purposes. $21 billion is a lot of capital to put to work, so the IDFC will need to make difficult upfront decisions about its equity operations and how it intends to deploy that capital. It might first consider niches where it has a comparative advantage serving particular funds, sectors, clients, or countries. In addition, the IDFC might want to consider the graduating sequence described above and seek temporary advisors seconded from other leading DFIs like the IFC or CDC that have performance histories and experience staffing and running equity investment operations. Many DFIs started their equity operations with just a few professionals who simply provided technical expertise as advisors to the DFI. We understand that OPIC has already engaged in this process, so it appears that the IDFC is already well on its way to creating a formidable equity division.

- See https://www.cgdev.org/sites/default/files/comparing-five-bilateral-development-finance-institutions-and-ifc.pdf

- See testimony given to the Senate Foreign Relations Committee on May 10, 2018 at https://www.foreign.senate.gov/hearings/modernizing-development-finance-051018. Although for a closer statistical look at the impact on multilateral DFIs in Africa from China's DFI investing money into various African countries ($97 billion from 2000 to 2014 and $12 billion per year since 2010), see https://www.aiddata.org/publications/china-in-africa-competition-for-traditional-development-finance-institutions

- These figures are as of 2017. See www.edfi.eu and each DFI website visited on February 9, 2019. For roughly equivalent figures from 2012 to 2016, similarly evidencing that DFIs are significantly weighted in debt rather than equity investments, other than the CDC, and that individual debt instruments tend to be larger in value than individual equity instruments, see https://www.cgdev.org/sites/default/files/comparing-five-bilateral-development-finance-institutions-and-ifc.pdf

- Equity includes quasi-equity like preferred stock and subordinated convertible notes.

- Debt includes other products like guarantees and political risk insurance.

- See https://www.brettonwoodsproject.org/2016/04/20508/

- See https://publications.iadb.org/publications/english/document/Comparative-Study-of-Equity-Investing-in-Development-Finance-Institutions.pdf