Following the 2023 bank failures, the federal banking regulators (the Federal Reserve, the OCC, and the FDIC) have signaled that they are seeking to develop more stringent bank regulatory requirements for larger banking organizations. These changes would range (or may likely to range) from regulatory capital, leverage and long-term debt, to liquidity and resolvability issues.

This resource provides a high-level, digestible summary of some the biggest changes proposed. Forthcoming coverage will focus on specific changes, industries and business lines, and institution types/sizes.

1. Capital

The federal banking agencies released a proposed capital rule in late July 2023 to revise the current U.S. capital rules applicable to banking organizations with more than $100 billion in total consolidated assets (including their subsidiary depository institutions) and those with significant trading activities. Banking organizations that meet those thresholds would generally include the following types of entities: banks and savings associations, bank holding companies and covered savings and loan holding companies, as well as U.S. intermediate holding companies of foreign banking organizations.

The Federal Reserve also released a separate proposed rule to amend its rule that identifies and establishes risk-based capital surcharges for global systemically important bank holding companies in the United States (U.S. G-SIBs).

2. Long-Term Debt

The federal banking agencies also issued a proposed rule that would generally require large banks and thrifts with total assets over $100 billion (and smaller banks and thrifts affiliated with them), as well as their holding companies, to issue and maintain outstanding a minimum amount of plain vanilla long-term debt that can be used to recapitalize these banking organizations in the event of their failure.

The federal banking agencies are attempting to improve the resolvability of these banking organizations, reduce costs to the FDIC's Deposit Insurance Fund, and mitigate financial stability and contagion risks by reducing the risk of loss to uninsured depositors.

While distinct from the current Total Loss Absorbing Capacity (TLAC) rule that generally applies to Globally Systemically Important Banks (G-SIBs) and their Intermediate Holding Companies (IHCs), the proposed rule would borrow many TLAC concepts and further harmonize the treatment of all large banking organizations with over $100 billion in total assets.

Please refer to our guide to the proposed long-term debt requirements.

3. Resolution Planning

The FDIC's proposed resolution plan rule would make significant changes to its current rule and would cover more banks—including banks that have been subject to a moratorium on filing for the past five years and some banks that may never have filed a resolution plan.

Unlike other recent proposals, the proposed resolution plan rule is not just limited to large banks above $100 billion in total assets. Instead, banks with at least $50 billion would be subject to certain substantial filing requirements that only nominally fall short of a full resolution plan in many respects.

(Our coverage of the proposed resolution planning rule will be forthcoming.)

Separately, the Federal Reserve also issued guidance for certain large bank holding companies that are required to file so-called living wills under the Dodd-Frank Act.

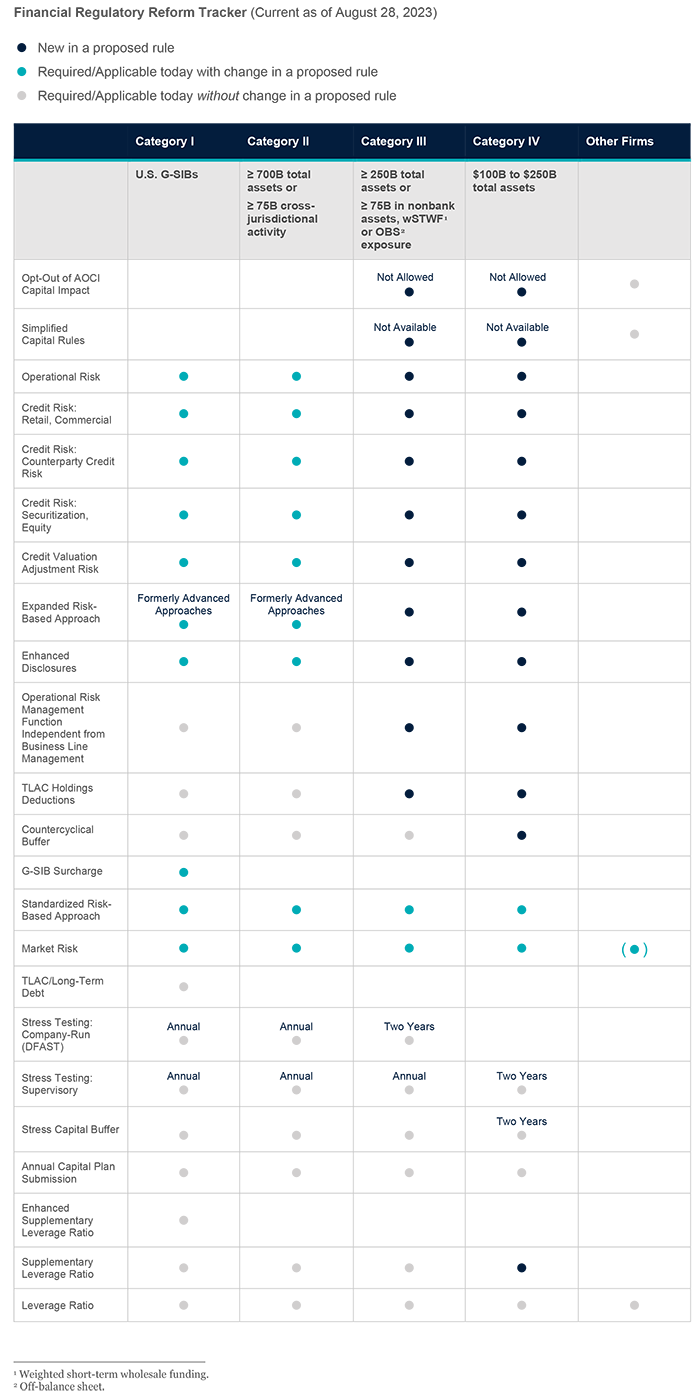

Financial Regulatory Reform Tracker (Current as of August 28, 2023)

![]() New in a proposed rule

New in a proposed rule

![]() Required/Applicable today with change in a proposed rule

Required/Applicable today with change in a proposed rule

![]() Required/Applicable today without change in a proposed rule

Required/Applicable today without change in a proposed rule

|

|

Category I |

Category II |

Category III |

Category IV |

Other Firms |

|

|

U.S. G-SIBs |

≥ 700B total assets or |

≥ 250B total assets or |

$100B to $250B total assets |

|

|

Opt-Out of AOCI Capital Impact |

|

|

Not Allowed |

Not Allowed |

|

|

Simplified Capital Rules |

|

|

Not Allowed |

Not Allowed |

|

|

Operational Risk |

|

|

|

|

|

|

Credit Risk: |

|

|

|

|

|

|

Credit Risk: |

|

|

|

|

|

|

Credit Risk: |

|

|

|

|

|

|

Credit Valuation Adjustment Risk |

|

|

|

|

|

|

Expanded Risk-Based Approach |

Formerly Advanced Approaches |

Formerly Advanced Approaches |

|

|

|

|

Enhanced Disclosures |

|

|

|

|

|

|

Operational Risk Management Function Independent from Business Line Management |

|

|

|

|

|

|

TLAC Holdings Deductions |

|

|

|

|

|

|

Countercyclical Buffer |

|

|

|

|

|

|

G-SIB Surcharge |

|

|

|

|

|

|

Standardized Risk-Based Approach |

|

|

|

|

|

|

Market Risk |

|

|

|

|

( |

|

TLAC/Long-Term Debt |

|

|

|

|

( |

|

Stress Testing: Company-Run (DFAST) |

Annual |

Annual |

Two Years |

|

|

|

Stress Testing: Supervisory |

Annual |

Annual |

Annual |

Two Years |

|

|

Stress Capital Buffer |

|

|

|

Two Years |

|

|

Annual Capital Plan Submission |

|

|

|

|

|

|

Enhanced Supplementary Leverage Ratio |

|

|

|

|

|

|

Supplementary Leverage Ratio |

|

|

|

|

|

|

Leverage Ratio |

|

|

|

|

|

Click here to download this chart.

{kind=link}

[1] Weighted short-term wholesale funding.

[2] Off-balance sheet.